The General License 42 and the authority of the 2015 National Assembly to renegotiate the Venezuelan external debt.

José Ignacio Hernández G.

Growth Lab, Harvard Kennedy School

*

As I explained in a piece published in CSIS, one of the problems related to renegotiating the Venezuelan external debt was the uncertainty about what polity is recognized as the Government of Venezuela in the U.S.

Between January 23, 2019, and January 3, 2023, the speaker of the 2015 National Assembly, acting as interim president, was recognized by the U.S. Government as the only polity with the authority to legally represent the Government of Venezuela, including the Republic and the national oil company (PDVSA). As a result of the sanctions imposed by executive orders, the interim president and the officials appointed by him required licenses from OFAC to represent the Government of Venezuela in the U.S., even regarding foreign creditors.

However, on January 3, 2023, the National Assembly disbanded the interim president. That day, the U.S. State Department (i) acknowledged that decision; (ii) reiterated the illegitimacy of the Maduros Government, and (iii) reinforced the political support to the 2015 National Assembly. Regarding the legal representation of the Government of Venezuela, it was clear that neither the speaker nor Maduro was deemed the president of Venezuela. It was unclear, though, if the National Assembly could be legally recognized as the Government of Venezuela.

Without a recognized Government of Venezuela in the U.S., creditors faced additional obstacles to advancing in renegotiating the legacy debt and, mainly, solving the problems related to the statute of limitations (SOL). The Maduro Government offered to extend the lapses of the SOL. However, the offer was useless because that Government does not exert legal representation of Venezuela and PDVSA in the U.S.

**

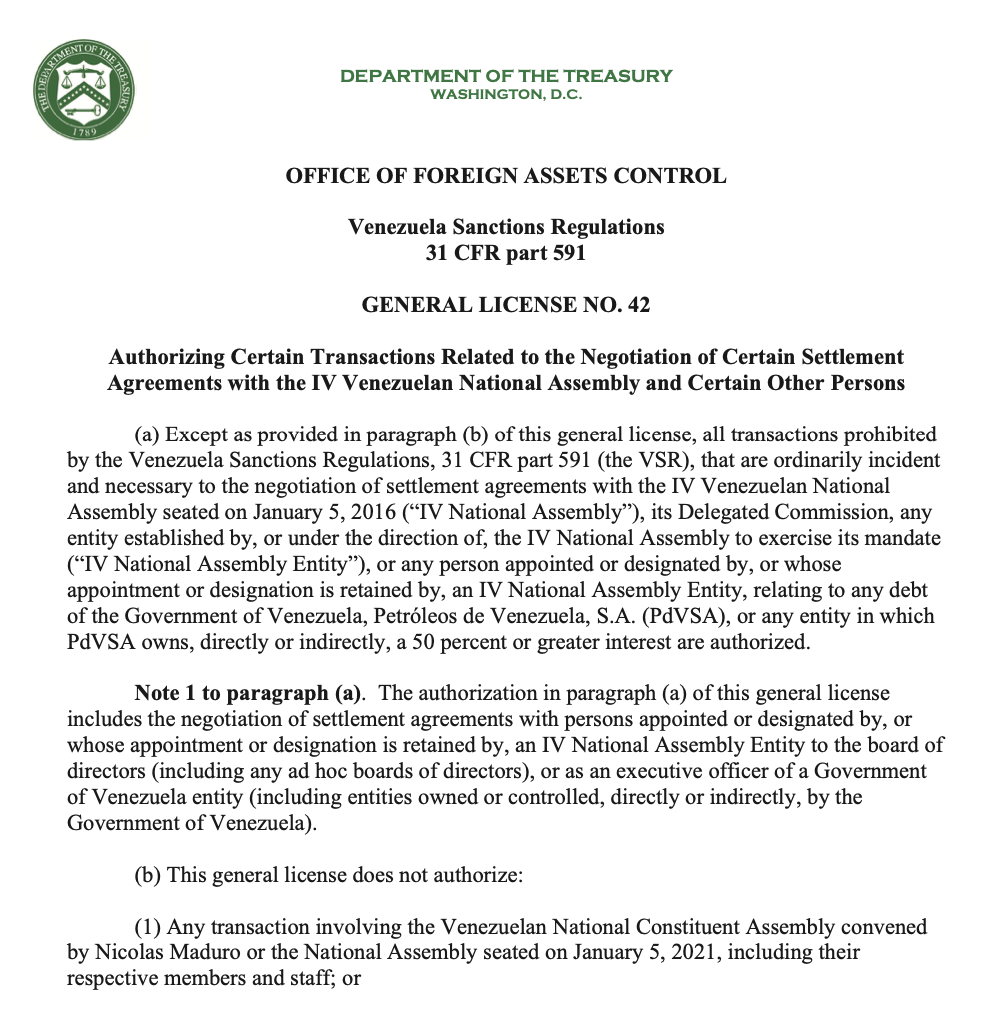

On May 1, 2023, OFAC issued the General License n° 42, authorizing the 2015 National Assembly and any organization it appointed to enter negotiations with creditors regarding the legacy debt. However, the GL does not authorize the entry into a settlement agreement -an action that will need specific licenses. Also, OFAC clarified that it “will not take enforcement action against any person for taking steps to preserve the ability to enforce bondholder rights to the CITGO shares serving as collateral for the PdVSA 2020 8.5 percent bond”.

Also, OFAC updated FAQ 808 to clarify that “creditors may file for writs of attachment without the need for OFAC authorization for matters involving property blocked “under the VSR.” This could mean that now U.S. Courts could issue writs of attachment, which enforcement will require a license, though.

There are at least two questions that arise from GL 42: (i) According to the U.S. Law, does the 2015 National Assembly legally represent the Government of Venezuela? and (ii) according to the Venezuelan Constitutional Law, can the 2015 National Assembly renegotiate the external debt?

The short answers to those questions are the following:

- According to U.S. Law, the recognition of foreign Governments is the exclusive authority of the Presidency. OFAC cannot recognize foreign governments; it only administers the sanctions program. Consequently, GL 42 is not a straightforward decision that recognized the 2015 National Assembly as the legal representative of the Government of Venezuela. However, it is a clear signal that, regarding the options between the Maduro Government and the 2015 National Assembly, the U.S. Government chose the National Assembly.

- The debt renegotiation is an exclusive attribution of the Executive Branch, based on Art. 236.11 of the Venezuelan Constitution. The Tittle III of the Organic Law for the Public Sector Financial Administration regulates the public debt as a responsibility of the Executive Branch, under the political control of the National Assembly (Arts. 80 and 82, which were regulated in Decree n° 3.425). Under the Venezuela Constitutional Law, the 2015 National Assembly cannot renegotiate the public debt because its role is to oversee and eventually authorize the debt renegotiation process, according to Art. 187.3 of the Venezuelan Constitution. This is why GL refers to an “executive officer of a Government of Venezuela entity“.

Consequently, GL 42 is insufficient to enable a transparent and lawful debt renegotiation process. From the U.S. perspective, it will be necessary to issue decisions that reinforce the authority of the 2015 National Assembly and the organizations appointed by it, to legally represent Venezuela and PDVSA. From the perspective of Venezuelan Law, the National Assembly must adopt the reforms that, following the Constitution, allow the legitimate Executive to represent Venezuela and PDVSA legally. In any case, the National Assembly must oversight and eventually authorize the debt renegotiation -which may require issuing special Legislation, as was outlined in the 2019 guidelines published by the then Interim President.

***

The legal problems that prevent the Government of Venezuela from advancing debt renegotiations in the U.S., particularly regarding the delicate situation of Citgo, are far from being solved. But GL 42 has paved the way for the 2015 National Assembly. It is necessary to complete the institutional reforms to solve the remaining legal problems.

The debt crisis, in any case, faced many challenges beyond those legal problems. Regarding the pending claims at the Delaware District Court and the 2020 Notes, the potential outstanding could be between 8 and 9 billion dollars. And this is just a small fraction of the Venezuelan external debt, estimated at no less than 140 billion. Those figures explained why the solution to the Venezuelan debt problem requires a broad political consensus that should be included in the political conversations between the Unitary Platform and Maduro -until now, only focused on external assets.

Besides, other contingent restrictions could be reviewed, such as the ban that prevents trading Venezuelan debt titles.

Since 2014, the comprehensive, orderly, and consensual renegotiation of the Venezuelan external debt has been waiting. It cannot wait too much. GL 42 could be the first step to finally addressing that problem.